“`html

How to Master Your Finances: Create a Bulletproof Budget That Works

Mastering your finances is one of the most important skills you can develop in life. It not only provides peace of mind but also sets you up for long-term success and financial freedom. At the heart of financial mastery is the ability to create and stick to a budget. A well-crafted budget is not just about cutting expenses or saving money; it’s about making intentional decisions with your money to align with your goals and values. In this article, we’ll explore how to create a bulletproof budget that works for you, not against you.

Why is Budgeting Important for Financial Success?

Before diving into the nitty-gritty of budgeting, it’s essential to understand why it’s such a critical component of financial success. Budgeting is the foundation upon which all other financial decisions are made. Without a clear understanding of where your money is going, it’s easy to overspend, accumulate debt, and struggle to achieve your financial goals.

- Tracks Your Spending: A budget helps you understand exactly where your money is going. This awareness is the first step toward making positive changes.

- Helps You Save: By prioritizing savings in your budget, you can build an emergency fund, save for big purchases, and work toward long-term goals like retirement.

- Reduces Debt: If you’re struggling with debt, a budget can help you allocate more money toward debt repayment and track your progress.

- Improves Financial Discipline: Sticking to a budget requires discipline, which is a crucial trait for achieving financial success.

How Do I Start Budgeting?

Starting a budget can feel overwhelming, especially if you’ve never done it before. However, with a clear plan, you can set yourself up for success. Here are the steps to get started:

Step 1: Assess Your Financial Situation

Before you can create a budget, you need to understand your current financial situation. This includes:

- Calculating Your Income: Start by figuring out how much money you have coming in each month. Include all sources of income, including your salary, freelance work, and any side hustles.

- Listing Your Expenses: Write down all of your regular expenses, including bills, groceries, transportation, and entertainment. Be sure to include both fixed expenses (like rent and utilities) and variable expenses (like dining out and hobbies).

- Identifying Your Debt: Make a list of any debts you owe, including credit cards, loans, and mortgages. Note the balance, interest rate, and minimum payment for each.

Step 2: Set Financial Goals

Your budget should be tailored to help you achieve your financial goals. Consider both short-term and long-term goals, such as:

- Building an Emergency Fund: Aim to save 3-6 months’ worth of living expenses in an easily accessible savings account.

- Paying Off Debt: If you have high-interest debt, such as credit card balances, consider prioritizing debt repayment.

- Saving for Big Purchases: Whether it’s a down payment on a house, a car, or a vacation, your budget should help you save for these expenses.

- Retirement Savings: Even if you’re just starting out, it’s important to begin saving for retirement. Take advantage of employer matching if it’s available.

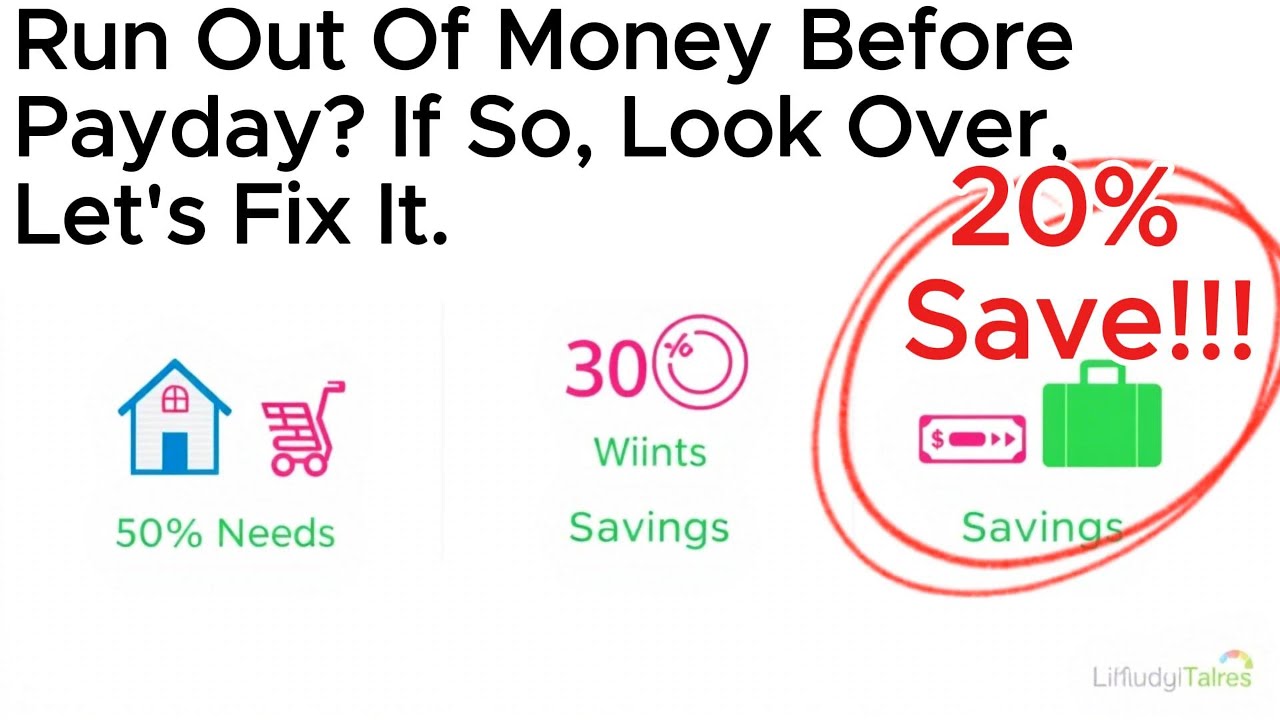

What is the 50/30/20 Rule?

The 50/30/20 rule is a popular budgeting framework that can help you allocate your income effectively. The rule suggests that:

- 50% of Your Income Should Go Toward Needs: This includes essential expenses like rent, utilities, groceries, and transportation.

- 30% Toward Wants: This category includes discretionary spending, such as dining out, entertainment, and hobbies.

- 20% Toward Savings and Debt Repayment: This portion of your income should be dedicated to building savings, paying off debt, and investing in your future.

While the 50/30/20 rule provides a good starting point, it’s important to adjust the proportions based on your individual circumstances. For example, if you’re trying to pay off high-interest debt, you may want to allocate more than 20% toward debt repayment.

How Do I Create a Budget That Actually Works?

Creating a budget that works requires more than just writing down numbers on a piece of paper. It requires a deep understanding of your financial habits, a willingness to make changes, and a commitment to tracking your progress. Here are some tips for creating a budget that actually works:

1. Use the Zero-Based Budgeting Method

Zero-based budgeting is a method where every dollar is assigned a job. This means that you start with a “zero balance” and allocate every single dollar toward a specific expense or savings goal. This approach ensures that no money is wasted and that every dollar is working toward your financial goals.

2. Prioritize Needs Over Wants

It’s important to distinguish between needs and wants when creating your budget. Needs are essential expenses that are necessary for survival, such as housing, food, and healthcare. Wants, on the other hand, are discretionary expenses that can be reduced or eliminated if necessary. By prioritizing needs over wants, you can ensure that you’re allocating your money in a way that aligns with your values and goals.

3. Automate Your Savings

One of the best ways to ensure that you stick to your budget is to automate your savings. Set up automatic transfers from your checking account to your savings and investment accounts. This way, you’ll ensure that you’re saving money regularly without having to think about it.

4. Track Your Expenses

Tracking your expenses is one of the most important steps in maintaining a budget. By keeping track of where your money is going, you can identify areas where you can cut back and make adjustments as needed. There are many tools available to help you track your expenses, including budgeting apps, spreadsheets, and even just a simple notebook.

5. Review and Adjust Regularly

Your budget shouldn’t be set in stone. Life is constantly changing, and your budget should change with it. Regularly review your budget to ensure that it’s still aligned with your financial goals and make adjustments as needed. This could mean increasing your income, reducing expenses, or reallocating funds to different categories.

What Are the Best Budgeting Tools?

There are many tools available to help you create and stick to a budget. The best tool for you will depend on your personal preferences and financial situation. Here are some of the most popular budgeting tools:

- Mint: Mint is a free budgeting app that allows you to track your spending, create a budget, and set financial goals. It also offers bill tracking and alerts for unusual account activity.

- YNAB (You Need A Budget): YNAB is a popular budgeting app that uses the zero-based budgeting method. It helps you assign a job to every dollar and stay on top of your finances.

- Personal Capital: Personal Capital is a financial management tool that allows you to track your income and expenses, as well as your investments. It also offers financial planning tools to help you achieve your long-term goals.

- Quicken: Quicken is a comprehensive personal finance software that allows you to track your spending, create a budget, and manage your investments. It also offers bill tracking and alerts.

- Spreadsheets: If you prefer a more hands-on approach, you can create your own budget using a spreadsheet. There are many free templates available online that you can customize to suit your needs.

How Can I Stick to My Budget?

Creating a budget is one thing, but sticking to it is another. It requires discipline, patience, and a commitment to your financial goals. Here are some tips for sticking to your budget:

1. Set Realistic Expectations

It’s important to set realistic expectations when creating your budget. If you try to cut your expenses too drastically, you may find it difficult to stick to your budget in the long term. Instead, make small, incremental changes that you can sustain over time.

2. Avoid Impulse Purchases

Impulse purchases can quickly blow your budget. To avoid them, practice delayed gratification. When you see something you want to buy, wait 24 hours before making the purchase. This will give you time to think about whether it’s something you really need or just a want.

3. Use Cash

Using cash instead of credit cards can help you stick to your budget. When you pay with cash, you can see the money leaving your wallet, which can make you more mindful of your spending. Consider using the envelope system, where you divide your expenses into categories and place the corresponding budgeted amount into an envelope for each category.

4. Celebrate Milestones

Celebrating milestones can help keep you motivated to stick to your budget. Whether it’s reaching a savings goal, paying off a debt, or simply sticking to your budget for a month, take time to acknowledge your progress. This will help you stay encouraged and committed to your financial goals.

5. Be Flexible

Remember that your budget is a tool to help you manage your finances, not a rigid set of rules. Life is unpredictable, and unexpected expenses will arise. When they do, don’t be too hard on yourself. Instead, adjust your budget as needed and move forward. The key is to stay flexible and adapt to changing circumstances.

What Are the Common Mistakes to Avoid When Budgeting?

While budgeting can be incredibly beneficial, there are some common mistakes to avoid. These mistakes can derail your efforts and make it difficult to achieve your financial goals. Here are some of the most common budgeting mistakes and how to avoid them:

1. Not Accounting for Irregular Expenses

Irregular expenses, such as car maintenance, property taxes, and holiday expenses, can catch you off guard if you’re not prepared. To avoid this, set aside a portion of your income each month in a separate savings account specifically for irregular expenses. This way, when these expenses arise, you’ll have the funds available to cover them without going into debt.

2. Overestimating Income

It’s easy to